LinkedIn

LinkedIn

WeChat

WeChat

Your supply chain’s well-being is our top priority. We at Maersk aim to provide you the most relevant and up-to-date information to help you navigate this period of heightened volatility.

Key Notes on North American Supply Chains

- Port labor updates: ILWU/PMA negotiations continue, though a tentative agreement was reached on health benefits. While the contract expired July 1, both parties have pledged to keep working at U.S. West Coast ports while negotiations shift to operational issues. In Europe, major Northern European terminals have been subject to frequent strike actions resulting in several stoppages across ocean and intermodal services. In Germany, further talks are planned for August 22nd between trade union ver.di and the Central Association of German Seaport Companies (ZDS). Port of Felixstowe dockworkers have called for an 8-day strike beginning August 21st at the UK’s largest container port, which may impact Transatlantic shipping.

- Presidential Emergency Board submits report and recommendations for stalled negotiations between rail unions and freight railroads: The National Mediation Board posted the PEB’s August 16th report, which included specific recommendations for wage increases. Work stoppages are prohibited for 30-days following the issuance of the report to give the parties time to reach a voluntary settlement. Congress can intervene if either of the parties reject the board's recommendations.

- Port Authority of New York and New Jersey Instituting “Container Imbalance Fee”: The East Coast’s largest port announced a new fee in its efforts to help clear the nearly 200,000 empty shipping containers that have built up around the port complex since the beginning of the pandemic. The PANYNJ’s fee is intended to incentivize ocean carriers to manage total outgoing port-wide container volume at levels equal to or exceeding 110 percent of its incoming container volume during the same period. The Port indicated that the empties are resulting in congestion, reduced chassis and trucker availability, and hurting terminal fluidity. The fee is to be effective Sep. 1st after a public comment period.

- Federal Maritime Commission seeks comments on benefits of issuing emergency order requiring information sharing: The FMC announced on 11 Aug that it is seeking public comment on whether current supply chain conditions warrant the issuance of an emergency order requiring common carriers and marine terminal operators to share key information with shippers, truckers and railroads. If the Commission issues an emergency order, common carriers and terminal operators would be required to share directly with relevant shippers, rail carriers, or motor carriers information relating to cargo throughput and availability. An emergency order would remain in effect for not longer than 60-days unless renewed.

- Updated hurricane forecast predicts “Above Normal” season: Extreme weather continues to impact supply chains globally. Now, for the seventh consecutive year, scientists are predicting an above normal season. The forecast indicates there could be 14-20 named storms with six to 10 turning into hurricanes that sustain winds of at least 74 miles per hour according to the National Oceanic and Atmospheric Administration. Shippers should understand their risks, review their plans, and be prepared for possible supply disruptions. Ninety percent of storm activity occurs between mid-August and October.

Ocean Update

Ocean container volumes continue to flow at substantial rates into the U.S. West and East Coasts as shippers have been proactively pulling a great deal of inventory forward to mitigate the impact of potential delays in the run up to peak shipping season. The Port of Long Beach reported its busiest July ever. Gene Seroka, Executive Director of the Port of Los Angeles, said that July was one of the “best on record” with improved cargo throughput. From a peak of 109 cargo ships waiting to enter the San Pedro Bay in January 2022, the current number of ships in the immediate vicinity has been worked down to around 10. In all, 58 ships are heading towards the bay.

Meanwhile, congestion has continued to build on U.S. Gulf Coast and East Coast ports, as well as at inland and rail terminals, which is impacting overall supply chain fluidity. There is a possibility that this congestion could increase during peak shipping season given the high number of existing import containers on terminals, building numbers of empty containers hindering operations, and long wait times for access to inland rail and other transportation resources.

We continue to stress the importance to customers that timely pick-up of import cargo is critical to alleviate terminal congestion. For its part, Maersk has been proactively taking steps along with APM Terminals to help keep key gateway terminals moving, including actions such as:

- Mobilizing a cross-functional task force of senior leaders to continuously develop and refine strategies for addressing supply chain congestion.

- Actively draying long-standing import containers to off-dock yards for key Los Angeles and Newark terminals.

- Offering long-term off-dock storage and transload solutions to customers with special requirements.

- Continuously offering Saturday gates at no extra cost to customers to reduce peak-hour traffic.

- Providing extra loaders to assist with empty evacuations, in addition to our normal vessel schedule.

- Removing damaged and end-of-service life containers from circulation.

- Investing in additional equipment, yard capacity, gate hours, and personnel to manage the increased volumes.

West Coast Highlights

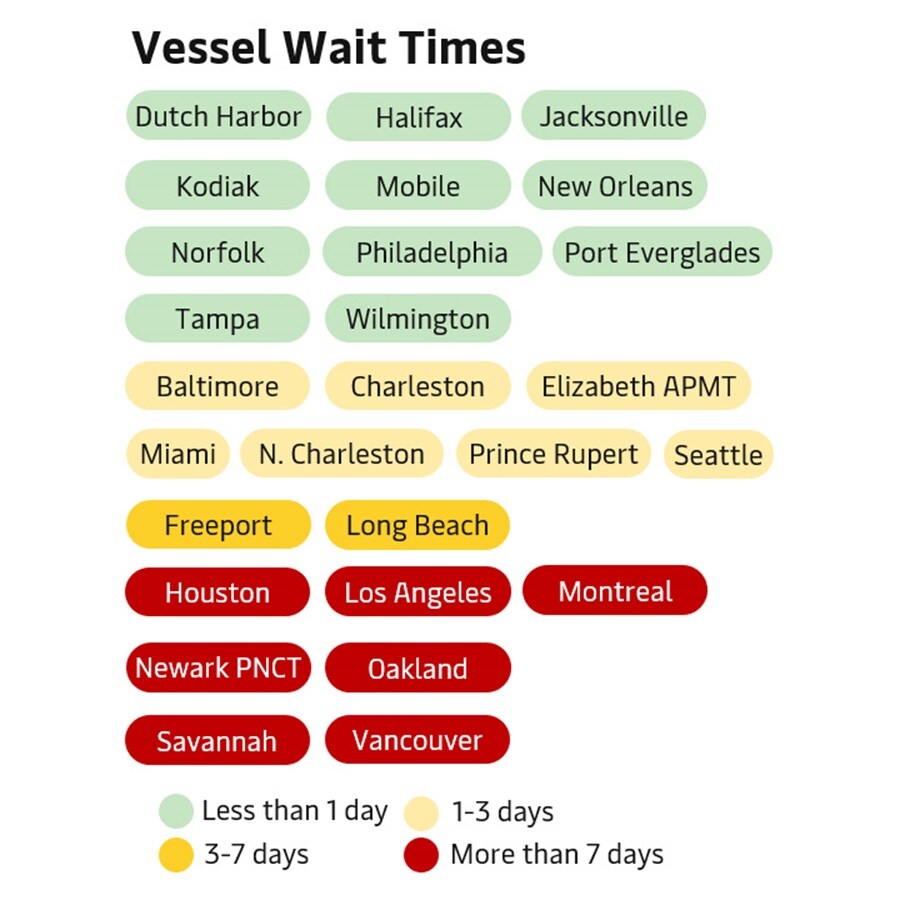

In the Pacific Southwest, 33 ships are heading to Port of Los Angeles and 25 are heading to Long Beach. Overall vessel wait times for LA now sit between 0-13 days with wait times of just 1-4 days for Long Beach.

Access to timely rail service continues to be a challenge. Overall rail dwell is 11.9 days in LA. According to Gene Seroka, about half of the 66,000 containers at the port are slated for on-dock rail with a volume that has increased six-fold since February. Approximately 50% of our network’s longstanding cargo units dwelling on terminal for 14 or more days are located in the Pacific Southwest ports.

Customers should continue to take advantage of Los Angeles Saturday Gates and second shifts when available. Effective Sep 1, the Port of Long Beach is removing the weekend exemption for free time in order to incentivize the use of expanded weekend gate hours.

Pacific Northwest

We continue to face operational challenges at Centerm in Vancouver. We are experiencing longer than usual vessel wait times for Transpacific services TP1 and TP9, as well as additional delays for the rail traffic due to the lack of space to discharge containers. To help alleviate the congestion, Maersk is currently taking the following actions:

- Alignment of eastbound TP9 sailings to match the cadence of Centerm’s contracted carrier service schedules.

- Evaluation of every TP9 vessel in the queue for possible changes to rotation. This includes calling Seattle first in the rotation when feasible.

- Calling at Prince Rupert for discharge of all Vancouver rail cargo.

- Actively pursuing other options such as transshipping over Seattle and utilizing other terminals in Vancouver including Delta Port and Fraser Surrey Docks.

In addition, we have adjusted our TP7 schedule by adding the ports of Prince Rupert and Surrey to aid with the terminal constraints in Vancouver as another alternative to our customers. While the situation remains fluid, we will continue to share updated Customer Advisories regarding the situation at Centerm allowing our customers to plan more effectively.

East Coast Highlights

For the past several months, East Coast congestion has been driven by both Transpacific market activity as well as a robust Transatlantic trade. Looking ahead to September, we are still seeing strong East Coast demand relative to the West Coast. As a result, port congestion remains and there have been delays on Transatlantic Services between North America and Northern Europe.

Vessel wait times are running 1-3 weeks in Newark PNCT, 1-3 days at APM Terminals Elizabeth, 2-18 days for Houston down in the Gulf, and 10-17 days in Savannah where 35 ships are at anchorage, five of which are Maersk vessels. To ease this congestion, we are arranging for extra gap loader ships in September where feasible for the East Coast.

The disruptions experienced on the North American and Northern European networks have required adjustments to our Transatlantic services, including resetting schedules. Currently, we are adding extra vessels to help reduce the time between departures. The extra vessels will avoid heavily congested terminals, such as Newark PNCT, and enable booking diversions to alternative locations such as Norfolk or Baltimore when possible. You can read our complete Transatlantic Services FAQ online for full details.

For all gateways, customers are asked to please provide their continued support in prioritizing the pickup of aging cargo as we work together with our terminal and rail partners to restore fluidity in operations for a more reliable supply chain.

Landside Update

“Just in Case” Inventory Management Driving Warehouse Space Availability to Historical Lows

According to real estate services firm CBRE, the vacancy rate for warehouses across the U.S. is down to 2.9%, a drop from 7.7% a decade ago. In the Pacific Southwest where 40% of America’s imported cargo enters the country, warehouse vacancy rates have dipped even lower — to around 0.5%. As a top 15 U.S. warehouse and distribution service provider, Maersk’s vacancy rates for its 20 million square feet of warehouse space across 80+ facilities are generally in keeping with the norm. There’s limited availability for the goods that keep coming through the system.

Having been caught short using long-practiced “just-in-time” strategies, retailers have responded to supply chain bottlenecks with “just-in-case” ordering strategies. This approach seeks to ensure stocks will be on hand when and where today’s demanding consumers want them. However, the net result of this shift has meant that warehouse capacity has become even more scarce. Complicating matters is that retailers placed these large orders many months ago thinking the pandemic boom would continue. In the interim, consumer spending shifted back to services while also slowing somewhat due to inflated prices. The result has been inventory surplus levels at multi-decade highs.

Customers looking to navigate the current challenges of today’s warehouse and distribution landscape are encouraged to plan and communicate with your supply chain partners well in advance. Additional warehousing capacity is under construction around the country, but not at the pace needed to alleviate the immediate supply chain pressures. Furthermore, today’s lead times of six to nine months to get inventories to market shelves are nearly double pre-pandemic planning cycles. In a rapidly evolving economy, this makes today’s forecasting decisions for next year’s markets particularly challenging. Finally, be sure to review inventory aging reports thoroughly to identify any stocks that may be approaching a disposition decision point.

Topics and Trends

Maersk Sees Global Container Demand Moving to the Lower End of its Forecast

In its Q2 Interim Report, Maersk reported that the demand for logistics services continued to moderate across global supply chains. Global container volumes declined by 2.3% in Q2, following a decline of 1.7% in Q1 2022 compared to Q1 2021. North American container imports from the Far East fell by around 1.0% in Q2, but overall levels remain elevated. Freight rates softened marginally over the quarter but remained at a high level historically as supply chain congestion increased across the globe.

In the United States, underlying demand held up more firmly in the quarter, but short-term indicators suggest weaker growth going forward, as exemplified by the deterioration of business and consumer sentiment in July. In response to inflation, the US Federal Reserve has been raising interest rates, adding further to downward pressure on overall activity.

Given this background, in 2022 Global container demand is projected to stay flat at the lower end of +/- 1% in 2022, but downside risks are prevalent. Supplier delivery times remain lengthy, and it is still uncertain when capacity constraints, including landside bottlenecks in trucking and warehousing, will abate.

Resources and tools to support you

Visit our “Insights” pages where we explore the latest trends in supply chain digitization, decarbonisation, growth, resilience, and integrated logistics.

Learn what’s happening in our regions by reading our Maersk Europe and Asia Pacific updates.

Visit us at Maersk.com to handle everything from "Last Free Day" to online payments.

We value your business and welcome your feedback. Should you have any questions on optimizing your cargo flows, please contact your local Maersk professional.

Get in touch

无论您需要什么,我们都可以随时为您提供帮助

解决方案

联系我们

准备好运送货物?

I agree to receive logistics related news and marketing updates by email, phone, messaging services (e.g. WhatsApp) and other digital platforms, including but not limited to social media (e.g., LinkedIn) from A. P. Moller-Maersk and its affiliated companies (see latest company overview). I understand that I can opt out of such Maersk communications at any time by clicking the unsubscribe link. To see how we use your personal data, please read our Privacy Notification.

By completing this form, you confirm that you agree to the use of your personal data by Maersk as described in our Privacy Notification.