LinkedIn

LinkedIn

WeChat

WeChat

Your supply chain’s well-being is our top priority. We at Maersk aim to provide you the most relevant and up-to-date information to help you navigate this period of heightened volatility.

Key Notes on North American Supply Chains

- Another railroad union rejects contract deal raising possibility of a strike or congressional action: The International Brotherhood of Boilermakers (IBB) is the third union to have rejected its tentative agreement with the US railroads. While there was a deal struck in September between the 12 unions representing 115,000 railroad workers and the National Carrier’s Conference Committee, select unions have continued to vote down the proposal in subsequent voting measures over quality-of-life issues. To date, seven unions have ratified the agreement with the BLET and SMART-TD unions to conclude voting on November 20th. The cooling off period is December 9th, after which time a potential strike could occur, unless Congress intervenes.

- ILWU / PMA negotiations languish on West Coast: West Coast ports continue to operate business as usual, though more than four months have lapsed since the labor contract expired on June 30th. Talks have been stalled for several months and industry officials do not believe talks will conclude until sometime in 2023. Talks have been delayed over an intra-union dispute between the ILWU and the International Association of Machinists and Aerospace Workers union over which workers at SSA Marine’s Seattle terminal get to perform a particular job function. The dispute was the subject of a National Labor Relations Board hearing that began on November 3rd and has since been adjourned, though will resume at the end of the month. Bargaining is expected to resume shortly between the PMA and ILWU.

Ocean Update

We continue to see signs of normalization in some markets. Overall trends for both East and West coasts look to be improving through the end of the year compared to October. The rate of cargo volume decline has slowed as customers are finalizing their 2022 shipping activity.

We are actively optimizing our network to meet available demand, which helps improve service quality in terms of frequency, reduced wait times and predictability. The intent is to keep goods flowing in an efficient manner while caring for the best possible outcome for the customers and stakeholders. Every effort is made to minimize impact to service delivery.

Customers should be mindful of the upcoming Chinese New Year holiday period, which begins on Sunday, January 22nd, 2023, and culminates with the Lantern Festival on February 5th. Maersk account teams are engaging customers as to how they will look to optimize their supply chains for this traditionally low-activity period – whether the strategy is to pull cargo forward as is the norm or to slow supply chains with post-holiday shipment activity.

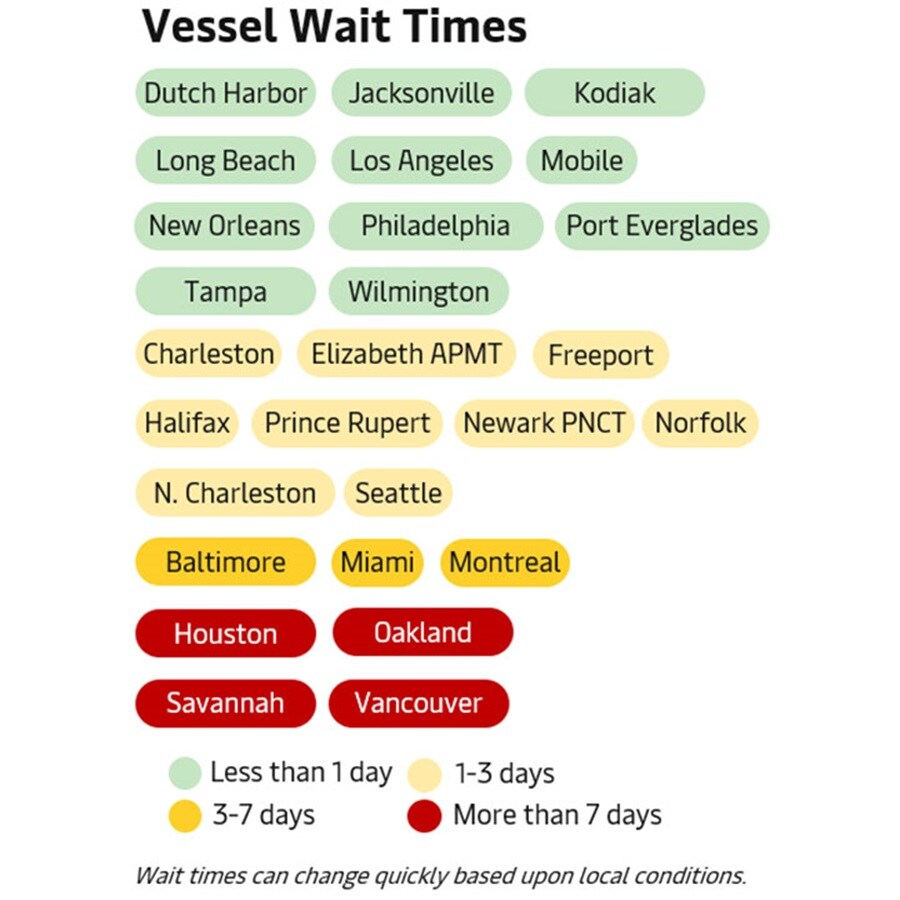

Network optimizations executed in the past month have begun to improve conditions, particularly in the Pacific Northwest. We continue to see the reduction of dwelling container units for both imports and exports. The top dwelling import locations are Baltimore, Prince Rupert, Houston, and North Charleston. The top dwelling export locations are Houston, Savannah, and North Charleston. Empty container availability remains good throughout North America and there are no issues for covering export demand. The longest vessel waiting times we are seeing are in Baltimore, Savannah, Houston, Oakland, and Vancouver. See details below.

West Coast Highlights

Oakland continues to struggle with labor shortages that are directly impacting operations, resulting in 10–12-day vessel waiting times. Status for the line-up, yard, and rail conditions remain impacted. Two of the port’s cranes were anticipated to be down for maintenance and repair for a week this month.

Congestion in Vancouver persists with line-up, yard, gate, and rail status all heavily impacted. Centerm is currently experiencing 20-day waiting times for TP1 and 38-days for TP9 services that connect ports in Northeast China and Busan, Korea, to the Pacific Northwest. With the combination of the TP1 and TP9 services into to a weekly service into Vancouver and Prince Rupert, we anticipate the reduction in vessel waiting time to drop to two-day waits.

East Coast Highlights

Houston is experiencing congestion with vessel wait times up to 12-days at Bay Port with its three available berths. Barbours Cut is experiencing 3-to-5-day vessel wait times for its six berths. Four Maersk vessels are at anchor. To address long-term container dwell, the Port of Houston announced a “Sustained Import Dwell Fee” that will be the responsibility of the owner of the cargo. However, while the fee was scheduled to begin December 1, the implementation has been postponed. The port will provide a 30-day advanced notice of the new effective date.

Congestion persists in Savannah: Class 1 vessels are experiencing 6-7 day wait times, while class 2 vessels are waiting up to 15 days for a berth. There are currently 30 ships at anchorage, four of which are Maersk vessels. Tropical Storm Nicole in early November delayed some activities at Savannah and other Southeastern ports. Savannah remains in a First In/First Out berthing pattern. Expect some improvement over the next weeks due to higher productivity forecasted before the upcoming holidays and decreased import volume.

Congestion in Baltimore is significant with yard storage above 95%. Vessel wait times for Transpacific routes stand at seven days, whereas wait times Transatlantic and Americas range from 3-5 days. The port is still operating on First In/First Out to reduce delays.

For Norfolk, the Port of Virginia announced a revised Early Receiving Date (ERD) policy effective Monday, November 7th. The ERD delivery window will now open 7 calendar days prior to vessel arrival, up from 5-days. This provides for a longer and more stable receiving window. We are also anticipating increased vessel waiting times of up to 10-days as port repairs are planned for cranes 6 and 7 at Virginia International Gateway (VIG). To mitigate the impact, we are changing some berths to Norfolk International Terminals (NIT).

Landside Update

What’s Driving Transportation “RFP” Season?

With the end of the year fast approaching, many businesses are looking to secure transportation capacity for 2023. Market conditions are changing rapidly, which has piqued the interest of transportation managers from coast to coast. We have noted increased transportation “Request for Proposal” (RFP) activity the past several weeks and expect the inquiries to continue into Q1. Top of mind for these logistics professionals is what capacity is available for the coming year? Can they find a new carrier to solve an old problem? And, of course, will they be able to find a more cost-effective solution to meet their transportation needs?

The incoming RFPs cover all things transportation, including first-mile drayage, truckload costs, and fulfilment. Customers are eyeing one-year contracts and looking beyond just rates to identify better overall partners and meaningful service level agreements (SLAs). Delivery times in the 97-98 percentile are key, and Load Tender Acceptance rates of 95% are highly desirable.

Long-term dedicated capacity has been of particular interest this RFP season as businesses have been prioritizing stability and the freedom to focus on the day-to-day business. Dedicated capacity is desirable as it saves the trouble of calling around for last minute capacity on the spot market. And while trucking capacity has opened up in the short term, the long-term driver shortage still persists, making dedicated capacity an important component of securing a reliable transportation network for the long haul.

RFP season is playing out against a new backdrop of market data. Researchers from leading logistics and supply chain schools recently published their latest market snapshot via the “Logistics Manager’s Index,” a survey that tracks industry trends over time. October LMI data points to an expanding logistics industry, albeit at a slower pace than previous months. Inventories remain high (though falling), warehouses remain relatively full, and costs are high. What has been changing though is transportation capacity. The LMI Transportation Capacity Index has reached an all-time high for LMI reporting, which dates back to 2016. Likewise, the Transportation Prices index began falling in April. In effect, the LMI data reflects the trend towards normalization of the transportation market to pre-pandemic levels.

Another indicator of trucking availability is the shift in national average for outbound tender rejections – a measurement that tracks how often trucking companies are rejecting haulage opportunities. Until recently, the figure had hovered around 9-10%, but has since dropped to just 5% according to FreightWaves. The increase in transportation capacity corresponds to the drop-off in inbound ocean freight during the past several months as many businesses pulled their shipments into the first half of the year to avoid a potential repeat of delays experienced during the pandemic. The October data indicates that retailers have begun drawing down warehouse stocks in anticipation of the holiday season, with reduced amounts of inbound containerized volume backfilling the space. The net result being that warehouse space has begun to open up, along with truck and chassis availability.

Topics, Trends & Insights

Be sure to visit our “Insights” pages where we explore the latest trends in supply chain digitization, decarbonisation, growth, resilience, and integrated logistics.

Maersk’s Take on the Market Situation

On November 2nd, Maersk released its Interim Report for the third quarter of 2022. In its press release, Maersk shared its view of the current market situation.

- Demand for logistics services moderated across global supply chains in Q3 2022

- Supply-side bottlenecks continued to pose challenges, but there are signs of easing as demand slows and COVID 19-related restrictions in China diminish

- Freight and charter rates declined in Q3 2022 relative to the previous quarter as the expected normalization gained momentum through the quarter

- Global container volumes are estimated to have declined –3% year-on-year in Q3 while global air cargo volumes, measured in CTKs, dropped by 9% in July/August (IATA)

- As a result of slowing economic activity, global container demand is expected to contract between –2 and –4% in 2022

In 2023, the global container market is expected to be broadly flat to negative, however given the current macroeconomic backdrop risks are skewed to the downside.

Customers can view the full report, press release, and other public documents on the Maersk Investor Relations page.

Resources and Tools to Support You

Learn what’s happening in our regions by reading our Maersk Europe, Latin America, and Asia Pacific updates.

Visit us at Maersk.com to handle everything from "Last Free Day" to online payments.

We value your business and welcome your feedback. Should you have any questions on optimizing your cargo flows, please contact your local Maersk professional.

Get in touch

无论您需要什么,我们都可以随时为您提供帮助

解决方案

联系我们

准备好运送货物?

I agree to receive logistics related news and marketing updates by email, phone, messaging services (e.g. WhatsApp) and other digital platforms, including but not limited to social media (e.g., LinkedIn) from A. P. Moller-Maersk and its affiliated companies (see latest company overview). I understand that I can opt out of such Maersk communications at any time by clicking the unsubscribe link. To see how we use your personal data, please read our Privacy Notification.

By completing this form, you confirm that you agree to the use of your personal data by Maersk as described in our Privacy Notification.