LinkedIn

LinkedIn

WeChat

WeChat

China’s October Golden Week, Christmas and Chinese New Year will bolster strong demand for container shipping for the last quarter of 2021. But port congestion, especially in the US and Europe, and service delays are expected to create headwinds for service schedules. Extra loaders and ad hoc port omissions will be implemented to help improve reliability. Factories in south Vietnam are scheduled to reopen from early October. The demand for air cargo and intercontinental rail across Asia remains strong while trucking demand in China is set to rise 10% ahead of the holidays.

This month, we share the latest market trend before highlighting the issues and challenges we face, and we also explain Maersk’s latest solutions to help you keep cargo moving.

Market Trend

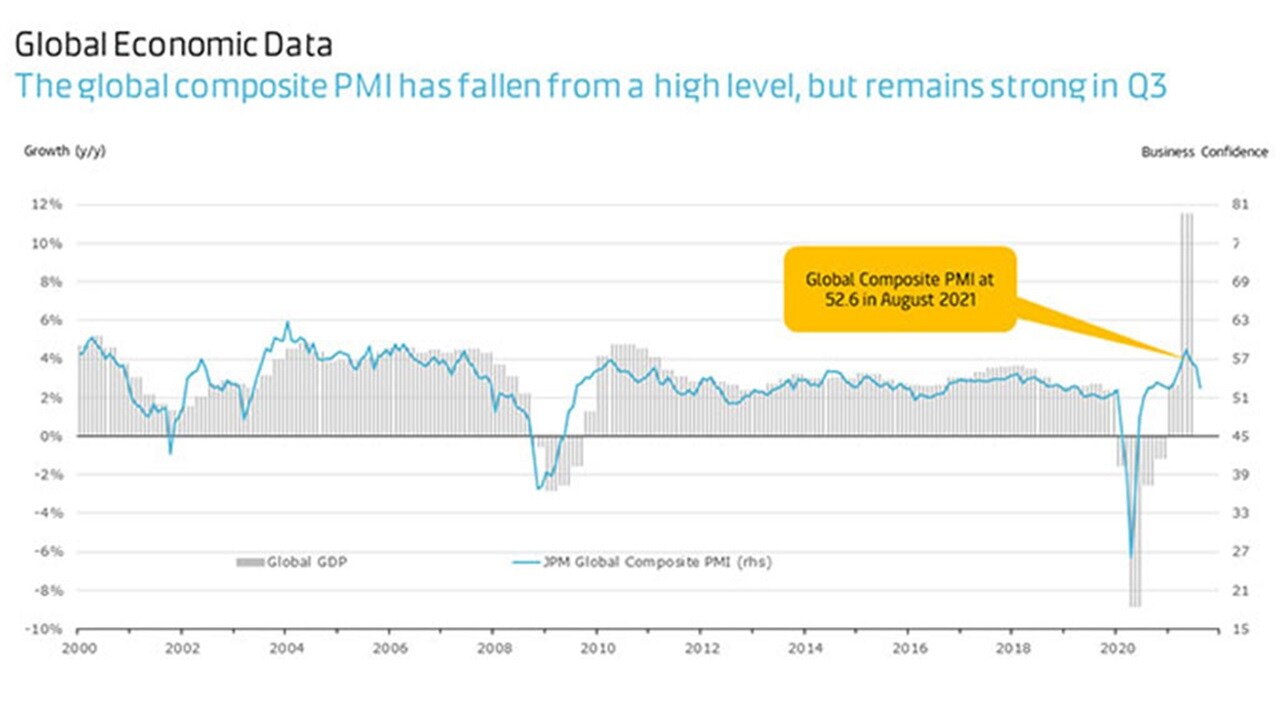

- The global economy remains robust although the pace of recovery has softened according to the global PMI manufacturing trends indicator. The global purchasing managers’ index hit 52.6 in August.

- Inventory levels in Europe and the US remain at their lowest levels on record, leading to stock outs on some products. This means even once retail demand declines, we will see cargo volumes continue to remain strong as inventory levels need to be rebuilt.

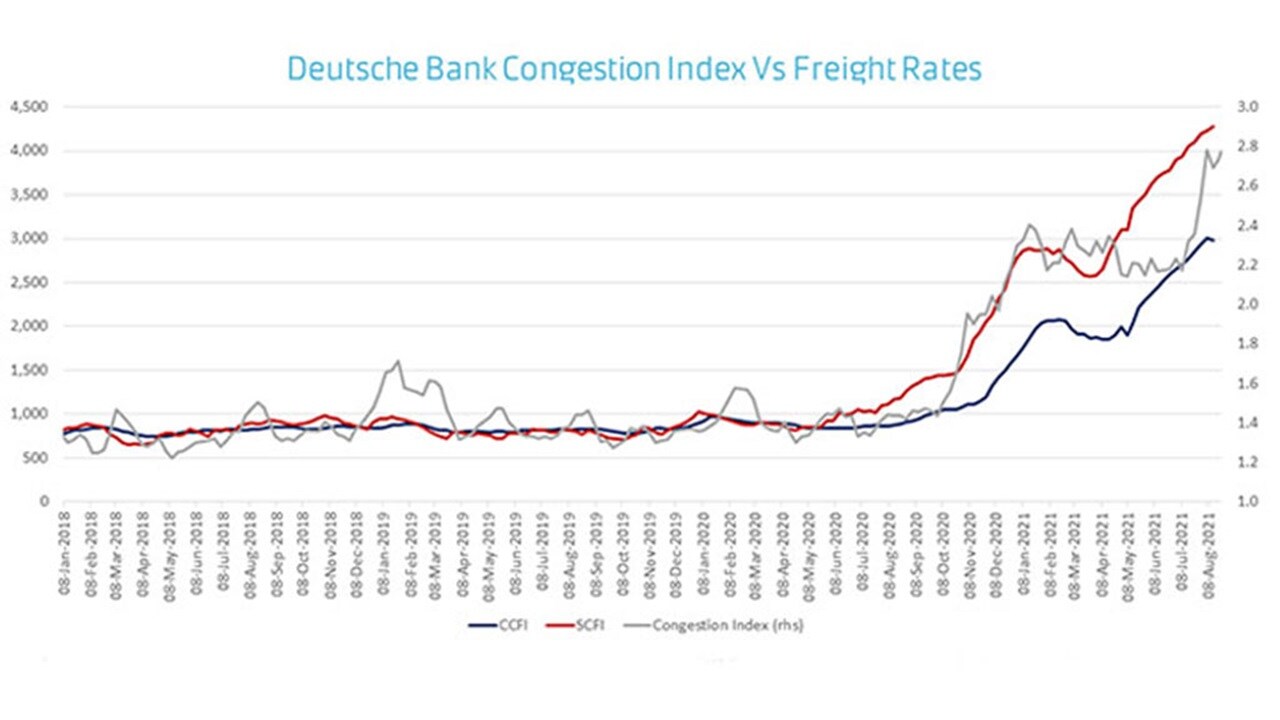

- Global container demand growth is projected at 6%-8% in 2021. The high 2021 forecast reflects the strong H1 as well as ongoing demand strength in the US and partly in Europe. Container demand growth ran ahead of supply growth in H2 2020 and into H1 2021, but the true drivers of high freight rates were congestions in ports and supply-chain bottlenecks including below factors:

- Capacity at ports: Vessel waiting time has increased requiring more ships per string to lift same cargo volume. At LA/long beach the waiting time has risen with 70+ vessels anchored in mid-September. Covid-19 led shutdowns have delayed vessels from Asia

- Warehousing capacity has been reduced due to port and landside congestion

- Returning empty containers back to Asia is challenging. Maersk has taken many actions to redirect flows back to Asia to ensure we have equipment supply. Despite this, equipment turn-round times continue to increase driven by landside and seaborne delays.

Trending themes

- How is Maersk addressing capacity and equipment shortages in the global supply chain?The COVID-19 pandemic has had an unprecedented impact on container shipping and global supply chains. Congestion at ports in the US, Europe and Asia as well, disrupted sailing schedules and equipment shortage, particularly in exporting countries such as in China and Vietnam, have created significant disruption for customers’ supply chains. Accumulated delays due to rapidly increased demand, COVID-19 control measures, lower productivity and poor schedule reliability are causing containers to remain in transit for longer, reducing the effective number of containers in active circulation.

Maersk has taken measures to alleviate this by rationalizing our schedules and repositioning the empty containers and we have tripled the number of dry freight containers in our fleet during the last few months to support our customers’ export requirements. However, In-fleeting of new containers alone is no longer sufficient to meet overall demand, so it remains critically important that import containers are turned around as quickly as possible. - The latest COVID situation in Vietnam

Hundreds of factories closed under lockdown rules are expected to reopen from early October, after Ho Chi Minh City authorities extended social distancing guidelines under Directive 30 until Sept. 30. City authorities also relaxed inter-district travel controls from Sept. 16 to allow deliveries of food and essential goods. Most key depots and ports are operating normally, but with lower productivity. The shortage of equipment and space is worse in the north than the south due to reduced cargo volumes.

Maersk’s airfreight services are operating normally although with longer transit times on some trade lanes. CFS warehouse operations in the south for outbound cargo resumed from Sept. 8, while inbound cargo handling was due to restart from Sept 20. Northern CFS warehouses are operating normally. Drivers need to show a negative test result within 3-7 days (depending on fast test or RT-PCR test) of moving cargo in/out of warehouses, depots and ports.

Ocean update

- We expect strong export demand from Asia to continue for the rest of the year particularly into the US and Europe. Several upcoming holidays including China’s Golden Week and Christmas will create seasonal volume rushes. We expect to see early signs of a pre-Chinese New Year rush in December.

- To improve schedule reliability, Maersk has decided to adjust vessel voyage numbers on Asia-North Europe services to match the corresponding actual weeks of departure. Continued strong demand, coupled with network disruptions has hammered our schedule reliability. Maersk will rationalize some of our service coverages to reduce the number of port calls to improve reliability. We advise customers to plan their supply chains well ahead, particularly for the upcoming holiday rush. Please click here to see the customer advisory.

- We expect Q4 to be stronger for Asia imports with network utilization remaining above 95%. We are striving to meet the needs of our import focused customers and reposition empty equipment back to Asia. As boxes remain in North America and Europe for longer, so the severity of container shortages increases across Asia.

- We expect equipment availability to continue to be tight in Q4 2021. We have increased our flow of empty containers into Asia ports, and invested in-fleeting of new containers to provide sufficient stocks for Q4. Our vessel schedules continue to be affected by port delays and we find it necessary to change some port rotations to reduce the total delays faced. Both the equipment and vessel schedule actions are specifically intended to improve reliability as far as possible. This chart here shows the current equipment status traffic for main loading ports in Asia. (Note: The equipment forecast is based on the supply and demand forecast, any increase in demand or supply delay would cause an earlier supply gap)

| Area | 20DRY | 40DRY | 40HDRY | 45HC | 40HCRF |

|---|---|---|---|---|---|

|

Area

China

|

20DRY

insufficient

|

40DRY

insufficient

|

40HDRY

insufficient

|

45HC

insufficient

|

40HCRF

insufficient

|

|

Area

Japan / Australia

|

20DRY

enough

|

40DRY

enough

|

40HDRY

enough

|

45HC

NA

|

40HCRF

enough

|

|

Area

Korea

|

20DRY

insufficient

|

40DRY

tight

|

40HDRY

insufficient

|

45HC

enough

|

40HCRF

enough

|

|

Area

Vietnam

|

20DRY

tight

|

40DRY

insufficient

|

40HDRY

insufficient

|

45HC

insufficient

|

40HCRF

insufficient

|

|

Area

Myanmar

|

20DRY

enough

|

40DRY

enough

|

40HDRY

enough

|

45HC

enough

|

40HCRF

enough

|

|

Area

Cambodia

|

20DRY

tight

|

40DRY

tight

|

40HDRY

tight

|

45HC

tight

|

40HCRF

enough

|

|

Area

Thailand

|

20DRY

insufficient

|

40DRY

tight

|

40HDRY

tight

|

45HC

enough

|

40HCRF

enough

|

|

Area

Malaysia

|

20DRY

enough

|

40DRY

enough

|

40HDRY

enough

|

45HC

enough

|

40HCRF

enough

|

|

Area

Singapore

|

20DRY

enough

|

40DRY

enough

|

40HDRY

enough

|

45HC

enough

|

40HCRF

enough

|

|

Area

Indonesia

|

20DRY

insufficient

|

40DRY

insufficient

|

40HDRY

insufficient

|

45HC

insufficient

|

40HCRF

enough

|

|

Area

Philippines

|

20DRY

enough

|

40DRY

enough

|

40HDRY

enough

|

45HC

enough

|

40HCRF

enough

|

|

Area

New Zealand

|

20DRY

enough

|

40DRY

enough

|

40HDRY

tight

|

45HC

NA

|

40HCRF

tight

|

- Key market outlook for trade lanes.

| Trade Lane | Market Outlook |

|---|---|

|

Trade Lane

Asia to Europe

|

Market Outlook

Market demand is expected to be strong and vessel space is very tight. Maersk is planning to reduce port calls to improve reliability and has contingency plans to mitigate the impact of equipment shortages in Yantian and Nansha and feeder capacity shortages in Southeast Asia.

|

|

Trade Lane

Asia to North America

|

Market Outlook

We expect strong demand to continue for the rest of Q4 but the overall North American ports situation has deteriorated recently. We expect the loss of capacity from missed sailings to continue. We have deployed gap loaders and launched new TP-X and TP20 services on USWC and USEC to bolster capacity and improve schedule reliability.

|

|

Trade Lane

Asia to Latin America

|

Market Outlook

The outlook through China’s Golden Week remains positive. We recommend customers divert cargo to North/East China ports if possible. Our focus continues to be on Non-Operating Reefer services to East Coast based ports, Chile and Peru.

|

|

Trade Lane

Asia to West Central Asia

|

Market Outlook

We expect strong demand to India in the coming month due to Diwali (Festival of Lights) in early November mainly driven by household goods. Space availability will be a key challenge.

|

|

Trade Lane

Asia to Oceania

|

Market Outlook

Market demand is expected to be strong in the coming months and capacity is tight. Congestion in Asia and Oceania ports continues to put pressure on vessel schedules, resulting in port omissions and missed sailings, which further exacerbates capacity availability. Our services are omitting some ports in Asia and Oceania to protect vessel calls at key origin and destination ports. We suggest customers plan their supply chains well ahead taking into consideration additional delays currently faced on the network.

|

|

Trade Lane

Oceanian Export

|

Market Outlook

Looking ahead into Q4 we see continued strong export demand out of Oceania. In the reefer sector, we expect reefer stocks to remain closely managed with demand continuing to exceed supply. Similarly, dry food quality containers are expected to remain in high demand with supply being managed within agreed allocations. The additional vessels deployed on our Oceania network remain key to ensuring network flexibility and absorbing schedule delays due to port congestion and high demand.

|

Air Freight update

- Overall market outlook: 2021 Q4 is expected to be one of the strongest peaks the industry has seen with demand surpassing 2019 levels. New technical product launches and winter fashion products together with continued ocean freight disruption are expected to push demand higher even as capacity has yet to return to pre-COVID levels. Rate levels, already at all-time highs, are set to increase further in Q4. Most of the major trade lanes such as transpacific, Asia-Europe and transatlantic will be impacted. Maersk is securing commercial airlines and ad hoc charters to address capacity issues and secondary airports to help overcome COVID-19 related airport restrictions. We are also offering our multimodal Sea-Air service to customers on the Asia-Europe trade lane to meet demand.

- Australia and New Zealand: Lack of capacity from China to Australia and New Zealand continues to put pressure on costs and transit times. Cargo from Vietnam to Oceania is experiencing delays due to capacity allocations to tech customers. Export cargo bookings from Australia to New Zealand remain under ad hoc terms for both capacity and rates due to very limited carrier options.

- Japan and Korea: Japan’s main airports including Tokyo Narita and Osaka Kansai have seen strong air cargo volumes in the last two months due to disruption in ocean shipments, with Kansai posting a 20.2% airfreight increase in August from a year earlier. South Korean airports saw 26.7% volume increase year-on-year in August, driven mostly by automotive shipments to US, China and Vietnam. As a ripple effect from additional airfreight disruption in China, rates both in Korea and Japan are increasing rapidly.

- Indonesia and Philippines: Strong export demand combined with reduced airline operations and services has resulted in tight capacity and high rates especially to US and Europe. Several airlines have reduced or cancelled flights from Jakarta. We expect air capacity will be constrained for the rest of the year.

- Vietnam, Cambodia and Myanmar: Rates are high and space extremely tight in the three countries due to strong demand and cargo delays at Asia airfreight hubs, with transpacific services the most critical. We suggest customers contact Maersk at least a month in advance to enable us to provide the right solution.

Landside update

- Greater China: Demand from large retail and lifestyle customers is fuelling a likely 10% increase in trucking demand in Q4. The usual capacity crunch due to the Christmas volume peak could be further impacted from pandemic controls across China. We encourage our customers to plan shipments earlier than previous years and provide rolling demand forecasts for trucking, rail and barges so Maersk can allocate equipment and capacity accordingly.

We anticipate Intercontinental rail demand will be much stronger in Q4 compared with last year but neither capacity nor equipment availability has significantly improved. ICR is also suffering from chassis shortages, border congestion and loading restrictions which are seriously impacting reliability. Customers should be prepared for long transit times and plan as early as possible. - Japan and Korea: Demand for ICR services in northeast Asia in Q4 will be stronger but there is a shortfall in capacity and equipment. We are working on potential capacity increases and products to cope with customers’ strong demand.

- Australia and New Zealand: Two services - Maersk Connect and Maersk Inland Storage – are helping customers overcome port delays and service omissions. Maersk Connect uses rail or road to move containers from port to port. Customers can use Maersk Inland Storage to move containers into storage to avoid large wharf storage charges.

- Vietnam, Cambodia, Myanmar: South Vietnam is expected to be out of a factory lockdown in early October which could result in a demand surge and capacity crunch. Demand for North Vietnam, Cambodia and Myanmar is expected to be strong for the rest of the year. With the container shortage escalating in North Vietnam, Maersk customers can choose one of three modes (trucking, barge and rail) to move containers from the south. An ICR with two block trains per week is now operating from Hanoi to Europe. There is also a rail service from Phnom Penh to Sihanoukville port in Cambodia.

Major port update

- Ports in Asia Pacific continue to be severely congested. With continued high yard density issue and weather disruption since July (i.e. 3 typhoons and 6 tropical storms), operational challenges remain in port operations and the situation is not expected to improve in the immediate future.

- Ports of Los Angeles and Long Beach congestion levels continue to deteriorate as we move further into peak season with 70+ vessels waiting at anchorage recently. Labour restrictions coupled with high throughput volumes remain the primary constraint.

- Port of Savannah has become increasingly challenging recently as congestion across the East Coast picks up. There were around 30+ vessels at anchorage with wait times upwards of 7 days in mid-September.

- Port of Seattle continues to struggle with available yard capacity. Waiting times have increased to 11/12 days and the typical port stay lengthening from 3 days to about a week.

- UK Ports are operating smoothly but with very severe trucking shortages across the country, leading to high yard density in ports. Port of Rotterdam is also seeing trucking shortages although not as severe as UK.

- Ports in Latin America: Port of San Antonio continues to be congested causing further delays. Port of Lazaro Cardenas - railways continue to be blocked by protestors. We suggest customers to move cargo to Manzanillo where possible.

Major ports update (Vessel waiting time indicator)

| Area | Less than 1 day | 1-3 days | More than 3 days |

|---|---|---|---|

|

Area

Asia-Pacific

|

Less than 1 day

Xiamen, Qingdao, Tanjung Pelepas

|

1-3 days

Nansha, Shekou, Hong Kong, Singapore, Port Klang, Sydney, Tauranga, Lyttelton

|

More than 3 days

Busan, Shanghai, Ningbo, Yantian, Auckland

|

|

Area

Rest of World

|

Less than 1 day

Charleston, Lome

|

1-3 days

Miami, Houston, Cotonou, Tema, Cape Town, Port Elizabeth, Balboa

|

More than 3 days

Antwerp, Rotterdam, Long Beach, Los Angeles, Oakland, Vancouver, Seattle, Prince Rupert , Savannah, Apapa, Onne, Durban, Dar Es Salaam, Sudan

|

For more information, please contact:

无论您需要什么,我们都可以随时为您提供帮助

解决方案

联系我们

准备好运送货物?

I agree to receive logistics related news and marketing updates by email, phone, messaging services (e.g. WhatsApp) and other digital platforms, including but not limited to social media (e.g., LinkedIn) from A. P. Moller-Maersk and its affiliated companies (see latest company overview). I understand that I can opt out of such Maersk communications at any time by clicking the unsubscribe link. To see how we use your personal data, please read our Privacy Notification.

By completing this form, you confirm that you agree to the use of your personal data by Maersk as described in our Privacy Notification.