LinkedIn

LinkedIn

WeChat

WeChat

With 2021 coming to an end, demand remains strong and the outlook for early 2022 remains cautiously optimistic even as global supply chains continue to face congestion and disruption issues and the ongoing Covid-19 pandemic poses wider economic challenges. The upcoming Chinese New Year between February 1-7 is likely to create a pre-holiday cargo spike especially as some South China barge services will be suspended. Shippers should also be aware of changes that are coming to HS customs codes. Looking longer-term, Maersk has decarbonisation as one of its strategic priorities having recently placed an order for a new generation of new dual-fuel container vessels.

This month, we share the latest trend before highlighting current challenges, and we also explain Maersk’s latest solutions to help you keep cargo moving.

Market Trend

The resilience of the global economy is being tested by inflationary pressures and the appearance of the new Omicron Covid-19 variant which is raising concerns about the effectiveness of worldwide efforts to control the virus. The Organisation for Economic Co-operation and Development (OECD) has outlined two possible scenarios facing the international economy from Omicron. The first scenario is it creates more supply disruptions and prolongs higher inflation for longer; the second scenario is more severe with governments again resorting to lockdowns and travel bans which could result in a decline in demand and inflation would fall faster. Fears about the impact from Omicron have already led to a sharp drop in crude oil prices by around $10 to $73 per barrel on December 1. The persistent increase in Covid-19 cases, especially in Europe, and uncertainty about the efficacy of vaccines to fight the Omicron variant has increased the threat of a more sustained slowdown in demand recovery.

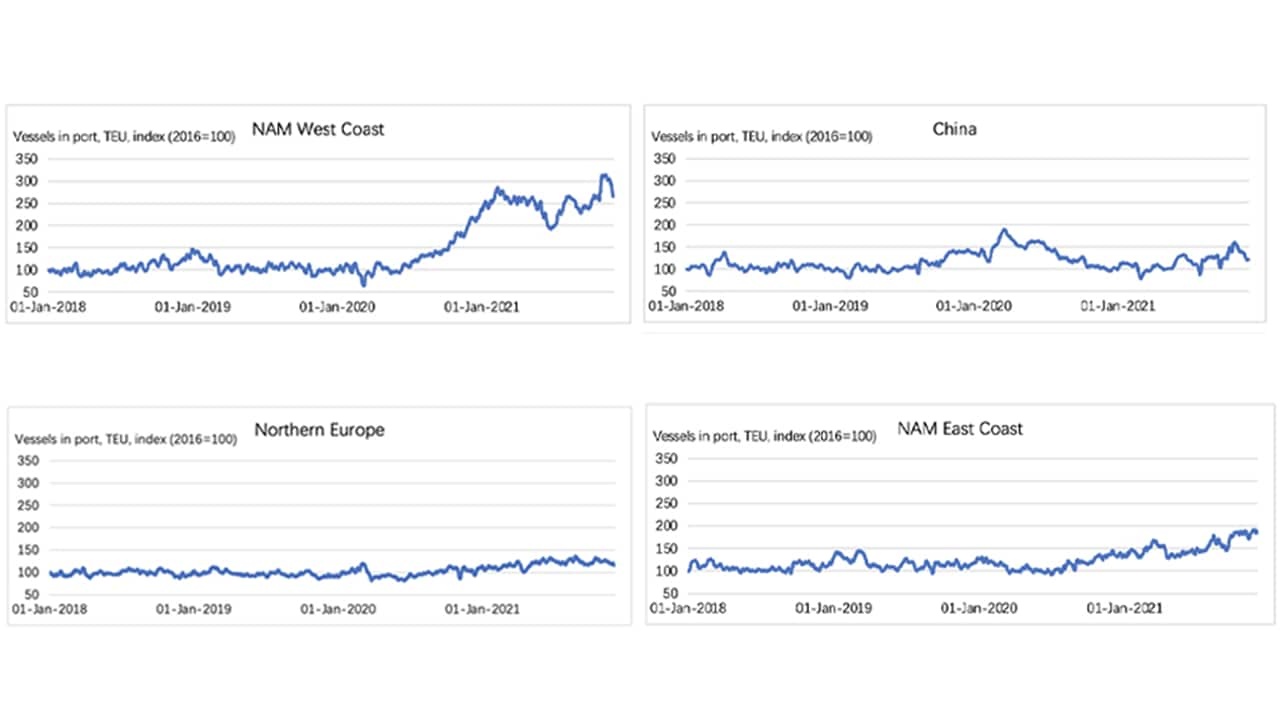

The container industry remained capacity constrained even as the global container trade grew 1% year-on-year in October. Landside disruption continued to substantially constrain supply chain capacity, while port bottlenecks reduced effective vessel capacity. The number of vessels waiting outside US West Coast ports is triple normal levels, while the number outside US East Coast ports has steadily risen over the last year. Vessel congestion outside ports in China and Europe has moderated.

Trending Topic

- Decarbonising logistics is one of our most important strategic priorities. Our actions have already made notable inroads towards that goal. By 2023, we will have the first methanol-enabled vessel on the water. We are working with logistics partners to develop a more comprehensive approach to fully integrate improved tools and processes when we engage with customers, suppliers and cross-sector partnerships. Click here to learn more about Maersk’s commitments on decarbonisation. To see what our methanol fuelled vessel designs look like click here.

- Changes coming to CHB. The Maersk HS code analysis tool includes changes that are coming to the Harmonized Commodity Description and Coding System from January 1, 2022. More than 350 provisions will be in place, impacting more than 1000 HS codes. It is critical to have the correct HS code classifications to ensure proper customs declarations for both export and import customs processes. The Maersk HS code analysis tool enables a thorough screening of your existing HS database and issues a report with details about commodities affected and recommendations on the right HS codes. This will help you proactively cope with the changes and avoid any compliance risks during the customs processes in 2022. For more information about the HS code analysis tool, please contact your Maersk CX and Sales teams.

- CNY Peak Season Preparation. Chinese New Year is the most important holiday in China impacting the global supply chain, it is also traditional peak season for exports from China (Feb, 1st for this year); Considering the latest situation of the pandemic, most factories are still watching on the developments especially local authority instructions to decide their production plan and holiday arrangements, the official instructions will be more clear in January. We expect strong demand and volume during 2022 Chinese New Year starting from this December, and the sporadically reported Covid cases in some areas may bring potential impacts to our customers’ supply chain; To ensure a smooth orders flowing during the CNY peak, Maersk Greater China has secured additional warehouse and landside transportation capacity for upcoming Chinese New Year peak season and will communicate closely with our customers on their shipping plans, one dedicated cross function work group will closely monitor the Ocean & Logistics service capacity, streamline internal teams for contingency plans on potential disruptions as well as on duty plan arrangements, meanwhile all our global customers will be shared the latest overall situation on regular basis.

Ocean Update

The rush before CNY is an important time for our customers, and we will be in-fleeting containers, returning empty equipment back to Asia at increased speed, and take strong measures to protect capacity – all to ensure we can be there for them in the best way possible through this period and beyond!

- Carrier capacity /equipment outlook for Q1: We expect space to remain tight through to CNY due to on-going capacity constraints due to sailing delays. There is expected to be tight supply of 40ft equipment, but there is a surplus of 20ft containers especially in greater China area although we will still see shortages in some locations ahead of CNY.

- Asia import and export demand and supply outlook: Demand remains strong and a significant order backlog will keep the export market full. The capacity lost due to delays means space will become even tighter in CNY. Overall import demand expects to remain at a similar level.

- Key Market Outlook across trades lanes

| Trade Lane | Market Outlook |

|---|---|

|

Trade Lane

Asia to North Europe

|

Market Outlook

Overall network capacity continues to be impacted by network disruptions. This will be especially critical until at least CNY. We aim to be agile with our network and clear cargo backlogs with extra vessels when possible. Schedules will be updated regularly to display the estimated ETAs/ETDs.

|

|

Trade Lane

Asia to Mediterranean

|

Market Outlook

To recover schedule reliability we will continue vessel slidings in December and January, further tightening capacity. Two gap loaders will be deployed in December and January to mitigate the capacity gap.

|

|

Trade Lane

Asia to North America

|

Market Outlook

We expect to continue to see a loss of capacity due to port congestion. We plan to deploy four gap loaders in December to mitigate the impact of missed sailings. As the North American ports situation is unlikely to improve for some time, we suggest customers increase the lead time between ETA and actual departure.

|

|

Trade Lane

Asia to Latin America

|

Market Outlook

There will be some controlled cargo rolling. Long wait times at origin and destination ports continue to put pressure on schedule reliability. For X4A, we are considering the bi-weekly omission of Busan/Hong Kong to ensure on-time vessel departures from Asia. The AC2 service will continue to omit either Yantian or Ningbo, while AC6 will omit Kaoshiung, Ningbo or Shanghai at origin and Balboa at destination to avoid further delay. For CNY, we suggest customers provide loading plans ASAP and explore using 20ft containers to facilitate early stuffing as stocks of 40ft equipment is projected to be tight.

|

|

Trade Lane

Asia to West Central Asia

|

Market Outlook

Capacity is expected to be tight. The FI4 service from East Coast India will depart every two weeks during December and January and is expected to resume weekly coverage from February.

|

|

Trade Lane

Asia to Africa

|

Market Outlook

The supply of 40ft equipment is tightening ahead of CNY and we suggest customers plan advance bookings and shift shipments into 20ft containers. There is a capacity bottleneck in North China which we are working to resolve.

|

|

Trade Lane

Asia to Oceania

|

Market Outlook

Long waiting times at origin and destination ports continue to put pressure on the network to maintain weekly sailings.

|

|

Trade Lane

Oceania Export

|

Market Outlook

Supply of 20ft reefer containers remains tight for Q1 and this is expected to continue during the 2022 export peak season. We recommend customer convert to 40ft reefers to avoid supply chain disruption. The supply of food quality containers remains tight in Oceania and a strong agriculture export season is expected in Australia. We have halted short-term booking acceptance for exports to South East Asian destinations to better manage cargo volumes through our Tanjung Pelapas hub during this high volume period. Space is forecast to be available for customers exporting general cargo from Australian East Coast to North East Asia and Greater China area.

|

|

Trade Lane

Asia Import

|

Market Outlook

Continuous vessel delays and port congestion are expected especially in Europe and North America which will negative affect cargo on-time delivery. The dedicated Cherry Express from Chile will be available on Week 51 and 52.

|

Air Update

- Greater China: Import capacity into China remains severely restricted as airports have prioritised ground handling to support export operations. Increased demand for test kits in Europe is becoming a key volume driver and increased volumes are likely to extend into January. Large numbers of charters are being arranged for test kit shipments.

- Australia and New Zealand: Qantas has temporarily suspended freighter services due to new Covid quarantine policies while Cathay Pacific has cancelled all cargo flights from Hong Kong SAR. This is impacting airfreight costs into Australia and New Zealand. China capacity continues to be extremely tight with airlines preferring to accept smaller volumes, or requesting bookings be split over multiple flights due to lack of space. Similar conditions continue to impact Vietnam flight operations with airlines accepting loose cargo only in small quantities. All bookings will be accepted at spot levels only due to daily fluctuations in both cost and capacity. Forwarders and shippers are considering charter flights for exports from Australia to New Zealand. Maersk will be exploring partial/full charter options for the remainder of the year to assist customers delivering New Year stock.

- Japan and Korea: Air cargo demand remains strong especially exports from Japan to North America although space from Northeast Asia to the US is tight with ground handing issues in the US delaying cargo. Space is expected to remain tight until Q2 2022 as forwarders divert cargo to air to overcome disruption to ocean freight. Forwarders are expanding regular charters to secure space for customers but rates have doubled or tripled forcing some shippers to switch back to ocean freight for Q1.

- Indonesia and Philippines: Capacity from Indonesia is tight. For bookings to the US and Europe we can book one week prior to departure for loose cartons although longer is required for skid cargo. Demand from the Philippines is still very high and capacity remains very limited. We suggest booking 1-2 weeks in advance to secure space although charter flights are an option for large volumes.

- Thailand, Malaysia, and Singapore: Demand from various verticals particularly from hi-tech, electronic and consumer goods continue to be high and outstrip current capacity. Trans-Atlantic rates continue to soar and is unlikely to stabilise for the next 1-2 months. TMS teams work with selected airlines on designated chartered routes to ensure lead time and capacity are achievable.

- Vietnam, Cambodia and Myanmar: Demand continues to exceed supply in all origins within VCM, while the US trade lane is the most critical trade with very high demand. Rates reflect the limited space and this is unlikely to change short-term. Ho Chi Minh airport is facing significant congestion and cargo backlog and customers are advised to send cargo forecasts in advance to help us plan space management especially for the last week of January ahead of the Lunar New Year that starts on January 30.

Inland Services Update

- Greater China: The shortage of drivers and road freight restrictions due to Covid regulations will impact available supply. We suggest customers plan CNY shipments and secure space as soon as possible. For cross-province/state transportation, customers need to check with shippers the specific local regulations regarding freight movements including driver vaccinations.

For China Intercontinental Rail Service, the overall market capacity is reduced in December especially between China and Europe. Border congestion is gradually improving. With Christmas and New Year approaching, trucking capacity in Europe could be challenging. To avoid excessive demurrage and detention charges, we encourage customers to plan deliveries as early as possible.

- Japan and Korea: We expect trucking volumes to increase ahead of the New Year which could increase congestion. But we anticipate congestion will worsen after the holiday when freight shipments resume.

The Maersk Inter Continental Rail service situation in Northeast Asia remains unchanged with very strong demand due to disruption in ocean transportation. But severe port congestion in Vostochniy has created significant delays. For Maersk’s IA1 service between Busan and Vostochniy, 5-7days are needed to berth and 3-5 days to load/discharge. Consequently, two voyages in November were postponed to arrive in December, which has created a cargo backlog in Busan. The backlog is expected to be clearly by early January and new rail service bookings have resumed for mid-January voyages.

Maersk acquired an Osaka CHB license on December 1 and we now operate our own Customs House Brokerage in three major ports - Yokohama, Tokyo and Osaka. - Australia and New Zealand: Oceania is witnessing storage challenges across the network with customer DC’s at capacity due to a combination of peak season demand and high inventory stocks. Our facilities are able to offer an immediate and agile solution for storage, fulfilment, deconsolidation to ease capacity issues in the supply chain. Port of Auckland has advised of pending industrial action in December.

Major Port Update

Major ports update (Vessel waiting time indicator)

| Area | Less than 1 day | 1-3 days | More than 3 days |

|---|---|---|---|

|

Area

Asia-Pacific

|

Less than 1 day

Qingdao, Xiamen, Lyttelton

|

1-3 days

Busan, Ningbo, Nansha, Hong Kong, Singapore, Tanjung Pelepas, Port Klang, Sydney, Tauranga

|

More than 3 days

Shanghai, Yantian, Shekou, Melbourne, Auckland

|

|

Area

Rest of World

|

Less than 1 day

Cape Town

|

1-3 days

Antwerp, Bremerhaven, Rotterdam, Newark, Charleston, Tin Can, Tema, Cape Town

|

More than 3 days

Felixstowe, Colombo, Long Beach, Los Angeles, Oakland, Vancouver, Seattle, Prince Rupert, Savannah, Houston, Apapa, Onne, Nacala, Dar Es Salaam

|

- Ports in China: Dalian Covid situation has increased the reefer yard density and restrictions on the pick-up of import frozen reefers remain unchanged. Reefer bookings to Dalian were closed from November 19 and remain in force. Barge services between Hong Kong SAR and South China will be curtailed from December 25 to February 10. Alternative transhipment services via Chiwan/Shekou or Nansha will be available.

- Ports in South East Asia: Tanjung Pelepas congestion remains critical, we continue to take action including rerouting cargo and keep monitoring inbound cargo flow via TPP. Philippines has limited space due to feeder restrictions into 2022.

- North European gateways remain congested with 2-3 days waiting time being the norm in Rotterdam/Antwerp/Bremerhaven. Felixstowe is still the most critical with high yard density of both empty and laden units. We are working with local teams to reduce pressure on Felixstowe as much as possible.

- Mediterranean: Algeria feeder space is restricted and facing overflow. Consequently, all the short-term services have been suspended until further notice. We continually face operational restrains at Haifa continually and services have been halted until further notice.

- Port of Savannah: 7-8 days waiting time. Average wait time will likely hold at around 8 days for the foreseeable future. US Flag vessel will be allowed to work on/close to their arrival p/forma. Vessel operations are being held mostly to a maximum of four-person gangs.

- Ports of Los Angeles and Long Beach: 25-30 days waiting time.

- Port of Seattle: 17 days waiting time.

- Port of Vancouver: 10 days waiting time

For more information, please contact:

无论您需要什么,我们都可以随时为您提供帮助

解决方案

联系我们

准备好运送货物?

I agree to receive logistics related news and marketing updates by email, phone, messaging services (e.g. WhatsApp) and other digital platforms, including but not limited to social media (e.g., LinkedIn) from A. P. Moller-Maersk and its affiliated companies (see latest company overview). I understand that I can opt out of such Maersk communications at any time by clicking the unsubscribe link. To see how we use your personal data, please read our Privacy Notification.

By completing this form, you confirm that you agree to the use of your personal data by Maersk as described in our Privacy Notification.